Cerebras Systems Faces Investor Uncertainty Despite Robust Revenue Growth

Cerebras Systems, the pioneering manufacturer of large-scale AI inference chips, has experienced a turbulent period since its much-anticipated IPO. Following robust Q1 financial results and the initiation of coverage by a leading Wall Street analyst, Cerebras’ stock (NASDAQ: CBRS) fell more than 3% on Tuesday, reflecting a complex mix of optimism and caution among investors. Despite headline-grabbing growth figures and strategic industry partnerships, a cautious outlook on gross margins and broader investment sentiment are shaping the narrative around this new public entrant in the AI infrastructure space.

Analyst Coverage and Stock Performance

On Tuesday, Cerebras Systems’ stock price dropped sharply, breaking further away from its peak and igniting discussions around valuation and future growth potential. The immediate trigger was a research note from Paul Meeks of Freedom Capital, who initiated coverage on Cerebras with a Hold rating and a price target of $209. Meeks’ stance was influenced by several factors, including the company’s recent margin guidance, its lumpy revenue growth pattern, and the inherent risks in such a rapidly evolving industry.

Since its Nasdaq debut on May 14, priced at $185 per share, Cerebras has seen significant volatility. The shares initially soared, reflecting market enthusiasm about AI hardware providers, but subsequently began to slide—briefly even trading below their IPO price last week. As of Tuesday, shares stood around $214, well below the 52-week high of $386.34 but above the low of $160.81.

Some analysts, like Meeks, had initially stayed on the sidelines, wary of the brisk post-IPO rally. However, the recent pullback shifted his perspective, even as he highlighted that risks still linger for investors, notably around the clarity of profitability as Cerebras scales.

Q1 Earnings: A Tale of Growth Tempered by Margin Concerns

Cerebras delivered its first financial results as a public company following the market close on June 23. The numbers, at first glance, painted a picture of breakneck expansion. First-quarter revenue climbed a staggering 92% year-over-year to $193.4 million, beating Wall Street’s estimates. The company’s net loss narrowed to $14 million from $23.9 million a year earlier—another signal that the business is maturing.

Driving these results was significant momentum in both key business lines. Hardware sales rose 60% year-over-year, totaling $111.6 million, as demand for the wafer-scale inference chips continued to surge. Meanwhile, the cloud services division delivered eye-catching growth, with revenues leaping 167% to $79.8 million.

However, investor enthusiasm was quickly tempered by Cerebras’ forward guidance on gross margins. While the company had managed to boost its quarterly gross margin from 42.1% a year earlier to 46.5% this quarter, it warned that the full-year margin would likely drop to a range of 38% to 41%. This guidance was seen as disappointing relative to both consensus expectations and the company’s own Q1 result.

Management attributed the temporary margin compression to a strategic decision: Cerebras opted to rent back some of its AI systems from an existing customer as it works to expand its own internal data center capacity. While the CEO emphasized to investors that this issue was transitory and tied to a specific business decision, the nuance failed to allay market apprehension, with many worried it could indicate deeper operational challenges amid scaling.

Business Model and Strategic Vision

Cerebras stands apart from many traditional semiconductor companies by manufacturing unusually large wafer-scale chips. These are not sold as standalone components, but rather as part of proprietary AI systems, complete with the specialized cooling and infrastructure required to support such powerful hardware. As AI demands evolve beyond what standard GPUs can deliver, Cerebras is positioning its hardware as a critical part of the future AI compute landscape.

Major Partnerships Fuel Growth Narrative

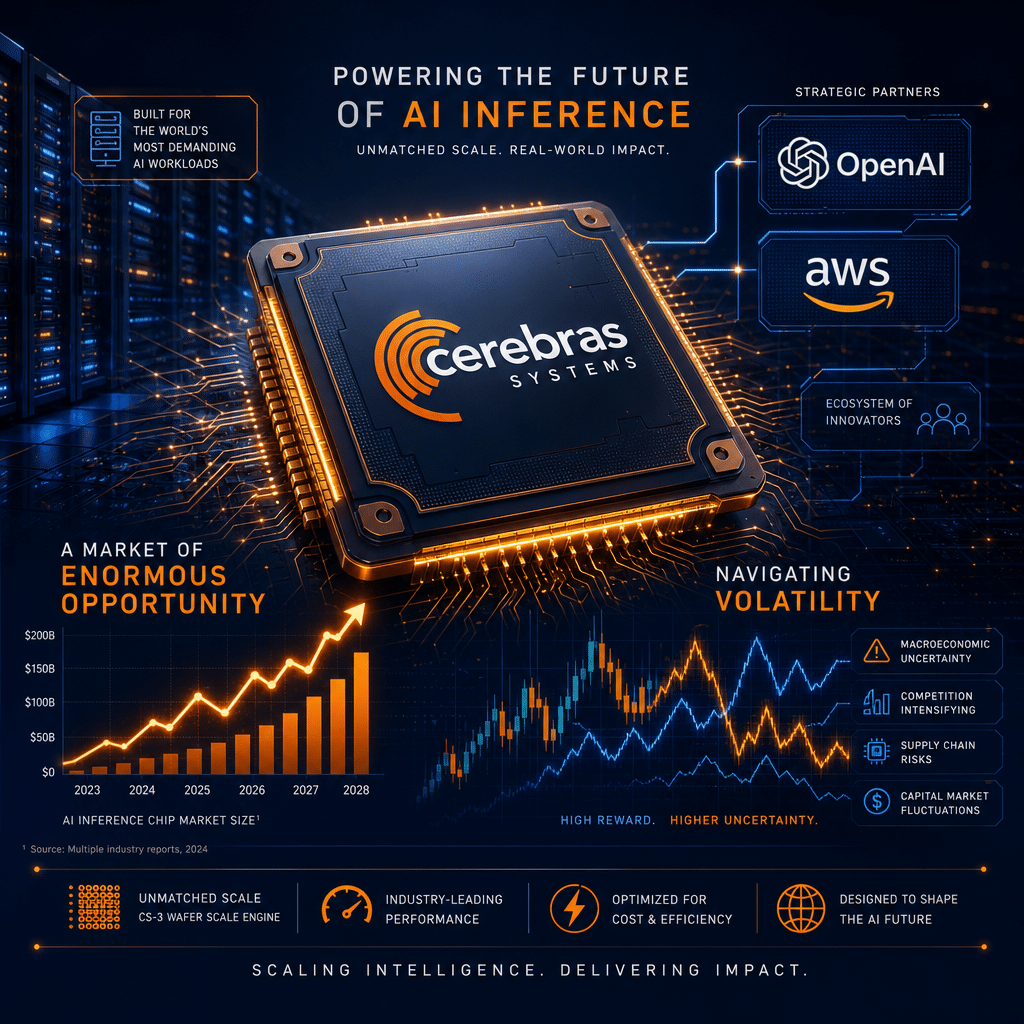

The company has crafted an impressive roster of high-profile partnerships. Perhaps most notably, in December Cerebras inked a multi-year, $20 billion agreement with OpenAI, one of the most influential players in the generative AI arms race. The deal is expected to provide not only steady revenue, but also a critical validation of Cerebras’ technological approach to large-scale AI inference.

In addition, Cerebras recently announced a partnership with Amazon Web Services (AWS), the world’s largest public cloud provider. This collaboration combines AWS’s in-house Trainium chips with Cerebras’ flagship CS-3 system, enabling the two to be co-located in AWS’s sprawling data centers for greater flexibility and performance in AI workloads. While Wall Street insiders note that meaningful revenue from this partnership may not materialize until 2027, it is widely viewed as a crucial foothold that could see Cerebras’ systems adopted at unprecedented scale in the cloud.

Market Trajectory and Analyst Outlook

Looking forward, Cerebras management has provided ambitious guidance for both the next quarter and the full year. For Q2, the company projects 88% year-over-year revenue growth, targeting $194 million. For the full fiscal year 2026, core revenue is expected to reach between $855 million and $865 million—a remarkable 69% annual expansion if the company delivers as promised.

Analyst Paul Meeks sees two primary drivers for Cerebras’ long-term success:

- System Sales: Direct sales of its CS-3 platform for inference-intensive AI applications are expected to anchor near-term revenue.

- Hyperscaler Partnerships: Cerebras is working with hyperscale clients—cloud titans like AWS—to pursue hybrid AI architecture, where GPUs from other manufacturers handle early-stage processing and Cerebras’ hardware accelerates the critical decode phase. This approach, if successful, could allow Cerebras to carve out a dominant niche in the evolving ‘AI factory’ model of enterprise compute.

Meeks also noted the risk-return calculus for investors has changed. The recent sell-off, he argues, has pushed out much of the speculative excess. However, he cautions that there’s no guarantee the stock’s recent low of $161 will act as a reliable support level. The path forward remains uncertain, especially if growth projections do not fully materialize or if macroeconomic headwinds slow technology spending.

Wall Street Consensus and Price Targets

Before Meeks’ Hold rating arrived, the Wall Street consensus on Cerebras had been overwhelmingly positive. Ten analysts rated the stock a Strong Buy, with an average price target of $299.30—implying a 44% upside from current prices.

This bullishness stems from Cerebras’ unique product positioning, formidable technology partners, and breakneck revenue growth. However, the stock’s fall from its high of nearly $386 underscores the reality that investors are closely watching for evidence of not just growth, but also sustainable profitability and operational resilience.

Risks and Opportunities Ahead

Cerebras’ ability to scale successfully in an increasingly crowded and fast-evolving AI hardware market will be critical to its long-term trajectory. The company’s reliance on several large customers, particularly OpenAI, presents concentration risk if any partnership falters. Furthermore, the specialized nature of Cerebras’ hardware—while a technical advantage—means the company relies on a high-touch, systems-integrator sales approach, with less volume and more lumpy deal cycles than more commoditized chipmakers.

On the flip side, if Cerebras delivers on its ambitious growth and margin targets, and if emerging partnerships like those with AWS translate into meaningful recurring revenue, the company may have substantial room to outperform not just analyst targets but also broader expectations for AI infrastructure suppliers.

The Broader Market Picture

The excitement around Cerebras is emblematic of the wider enthusiasm (and caution) pervading the AI hardware investment space. As generative AI and large language models demand ever-greater computational power, the race for innovative hardware solutions is intensifying. Cerebras’ approach—giant chips for specialized inference tasks—fits squarely into this trend, but it also raises questions about scalability, interoperability, and cost.

Investors are keenly aware of both the potential for outsized rewards and the specter of volatility that have accompanied many recent tech IPOs. In this context, Cerebras’ impressive revenue growth, marquee customer wins, and evolving valuation will continue to be scrutinized as new data emerges.

Conclusion: A Promising But Uncertain Road Ahead

Cerebras Systems has captured the market’s attention with its technological innovations, industry-defining partnerships, and explosive revenue growth. Yet, its post-IPO journey highlights the challenges of navigating public markets amid sky-high expectations and the unforgiving scrutiny of quarterly earnings. For now, investors appear to be balancing the company’s considerable opportunity with healthy skepticism about near-term margin pressures and execution risk.

The next few quarters will be pivotal. Investors will be watching closely to see whether Cerebras can not only meet its ambitious growth forecasts, but also demonstrate sustainable improvement in margins and profitability. The company’s trajectory—both as a stock and as an enterprise—will serve as an important bellwether for the future of AI infrastructure investment.