Nvidia (NVDA) has long been a focal point of the stock market, especially as artificial intelligence (AI) and next-generation chip technology reshape the global economy. Renowned for its innovation and dominance in both gaming and high-performance computing, Nvidia’s stock has encountered a volatile ride in recent months, leading many investors to reassess its prospects. In this article, we take an in-depth look at the latest developments affecting Nvidia’s stock: performance, earnings, institutional actions, analyst forecasts, and potential risks as the broader tech market evolves.

Recent Stock Performance: A Mixed Bag

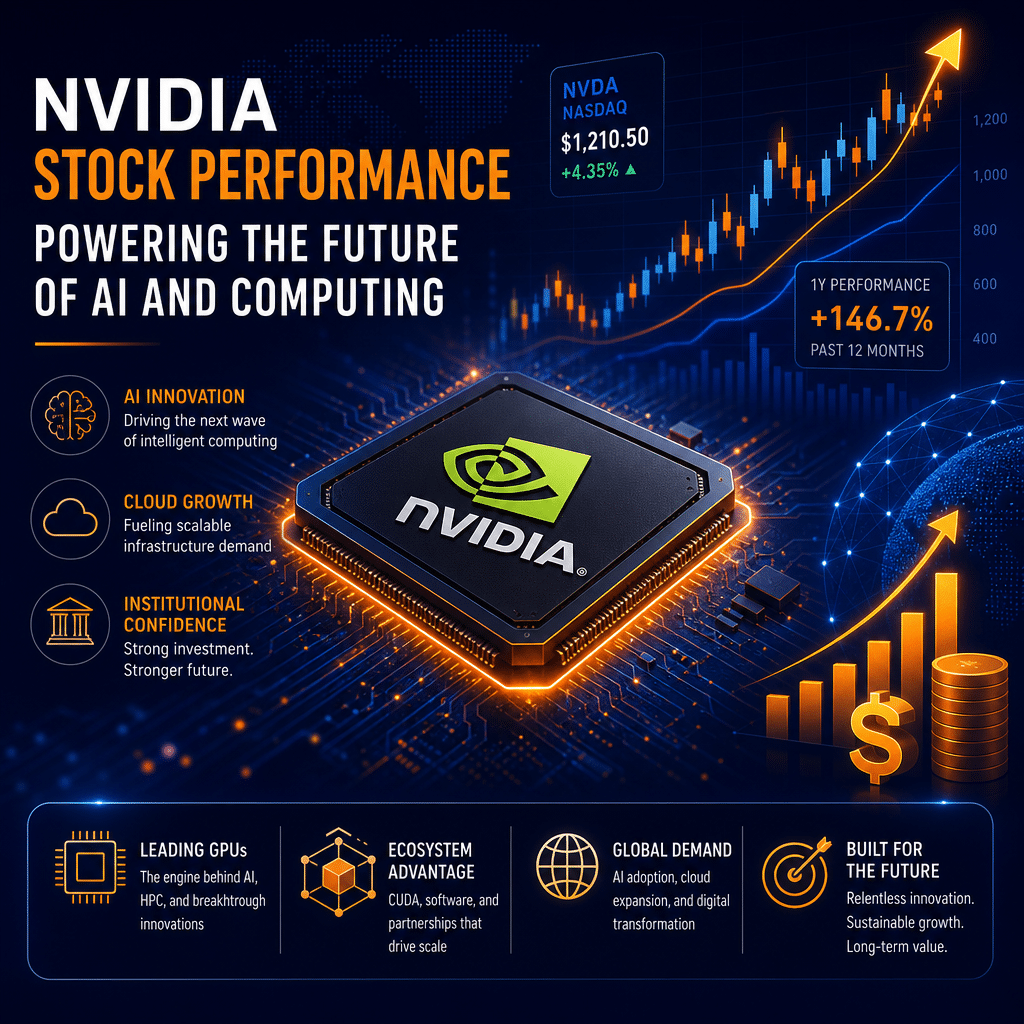

As of Friday’s open, Nvidia shares traded at $192.53, capping off a challenging stretch in which the stock fell nearly 9% over the preceding month. This lackluster momentum contrasts sharply with the rapid gains investors had come to expect in the years prior. Year-to-date, NVDA boasts only a modest 5% uptick, suggesting a cooling off after a period characterized by exponential growth.

Key to understanding this performance is the compression of Nvidia’s forward earnings multiple. The stock now trades at roughly 22 times forward earnings, down dramatically from almost 40 times in July of the previous year. On the surface, this contraction presents the stock as more reasonably valued—potentially an opportunity for bargain hunters. Still, the wider context of market dynamics, sector cycles, and competition must be considered before declaring NVDA a clear buy.

Institutional Activity: Big Money Moves Show Confidence

Despite recent dips, institutional investing in Nvidia points to enduring confidence from some of the world’s largest asset managers. Generate Investment Management, a prominent institutional investor, increased its position in Nvidia by an impressive 62.5% during the first quarter, purchasing over 533,000 additional shares. This commitment brings Generate’s total holding to nearly 1.39 million shares—now representing 11.9% of its portfolio, making NVDA its largest single position. At press time, this holding is valued at approximately $241.7 million.

Other major institutions have similarly boosted their Nvidia exposure. Norges Bank, holding roughly $62.2 billion worth of the tech giant’s shares, joined the ranks of new institutional investors. Meanwhile, J. Stern & Co. increased its position by over 13,700%, and Cardano Risk Management multiplied its stake by nearly ninefold. In total, institutional investors collectively own approximately 65.27% of Nvidia’s outstanding shares, signaling robust institutional faith in the company’s future trajectory.

Impressive Earnings and Capital Return Strategy

Underpinning some of this institutional enthusiasm is Nvidia’s outstanding recent earnings report. For the most recent quarter, the firm delivered earnings per share (EPS) of $1.87—beating analyst expectations of $1.76. Revenue came in at a formidable $81.61 billion, dramatically exceeding the $78.42 billion consensus and marking an 85.2% increase year-over-year. For a company of Nvidia’s scale, such growth is particularly noteworthy, affirming its central position in the rapidly growing AI and data center chip markets.

Additionally, Nvidia’s board has approved a significant $80 billion share buyback program, while also raising its quarterly dividend from $0.01 to $0.25. This marks a notable shift in the company’s approach to capital return, rewarding shareholders not only with potential price appreciation but also with an attractive, albeit still modest, dividend yield. In an era where tech stocks are often criticized for minimal capital returns, Nvidia’s more shareholder-friendly posture could help broaden its investor appeal.

Wall Street Sentiment Remains Strong

Analyst confidence in Nvidia remains robust, with a broad consensus rating of “Buy” among 54 covering analysts. The average price target sits at $303.84, over 50% above Friday’s opening price and indicating that Wall Street sees significant upside potential. Jefferies, a well-known brokerage, recently raised its target to $300, while Chinese investment bank CICC hiked its own target to $268.30. Analysts continue to cite Nvidia’s commanding position in AI chips, data centers, and high-margin verticals as grounds for their bullishness, even as the broader tech sector faces valuation and growth challenges.

Risks and Headwinds: What Investors Need to Watch

Despite the many strengths, there are several reasons for caution when it comes to NVDA’s near-term outlook. First is the aforementioned compression in its forward earnings multiple. While these lower multiples can indicate a more rational valuation relative to projected earnings, they may also foreshadow stiffer competition and thinner industry margins—hallmarks of cyclical hardware markets.

The high-growth chip sector is notoriously vulnerable to competition, and major cloud providers such as Amazon, Google, and Microsoft are all investing in custom AI silicon. Rivals like AMD and Intel remain formidable, each bringing new technologies to market that could erode Nvidia’s share of the pie or force price reductions to maintain dominance. As the AI hardware arms race intensifies, Nvidia’s premium pricing and margin resilience may be tested.

Another red flag for some investors is recent insider selling. Notably, Director Mark Stevens sold 885,000 shares on June 18 at an average price of $210.17—a staggering $186 million transaction, reducing his position by over 14%. In late May, Director John Dabiri also sold 625 shares at $214 per share. Over the past three months, insiders have collectively sold more than 1.9 million shares, valued at approximately $410.6 million. While insider sales are not always a sign of impending trouble (often triggered by personal financial planning or diversification), heavy selling can sometimes precede price corrections or signal a perception of peaking valuations.

Technical Analysis and Market Statistics

Examining Nvidia through a technical lens adds another dimension to the story. One technical model projects that NVDA’s shares are likely to trade between $190 and $225 over the next ten weeks, with a median five-week target of around $213. This predicted range is consistent with the stock’s recent volatility: Nvidia has posted only four up weeks out of the last ten, reflecting the choppy trading that has characterized the market of late.

The stock’s 52-week range stretches from $151.49 to $236.54, underscoring both its significant rally off 2023 lows and its susceptibility to selloffs. With a current market capitalization of $4.66 trillion and a 200-day moving average hovering around $193, Nvidia sits at a technical crossroads—potentially poised for recovery or susceptible to further retracement if sector sentiment sours.

Valuation in Context: Is Nvidia Stock Cheap or Overhyped?

For value-oriented investors, the contraction in Nvidia’s earnings multiple is an encouraging development, making the stock appear more reasonably priced relative to its peers. At 22x forward earnings, Nvidia is less “expensive” than it was at 40x, but that doesn’t mean the stock is truly inexpensive—especially considering its dominant market share, rapid innovation, and AI-driven upside.

However, there are risks that the multiple could stay suppressed if market participants shift from growth to value, or if Nvidia faces significant competitive pressure. Additionally, cyclicality in semiconductor markets can quickly reverse fortunes. Nvidia’s continued ability to innovate, capitalize on AI, and outpace rivals remains vital for it to justify elevated expectations.

Nvidia’s Strategic Pivot: Capitalizing on AI and Data Centers

Central to Nvidia’s bullish thesis is its unmatched role in AI computing. The company’s graphics processing units (GPUs) are at the heart of most generative AI models, data center operations, and high-performance computing applications. Nvidia’s AI hardware has become indispensable to global tech giants, scientific research, and startups seeking computing horsepower.

Nvidia’s shift toward recurring revenue—via software, services, and cloud partnerships—also offers a buffer against hardware cyclicality. Its CUDA programming platform and ongoing investments in AI software ecosystems further diversify its offerings and erect barriers to entry for would-be rivals.

Conclusion: A Balanced View for Investors

Nvidia remains one of the most important names in technology, straddling multiple lucrative sectors and leading the charge in the AI revolution. Its recent earnings blowout, strong institutional backing, and robust analyst support paint a picture of a company with ample near-term upside and long-term promise.

However, investors should not ignore signs of market maturation, increased insider selling, and growing competitive threats. As valuation multiples recede, Nvidia’s results—and its ability to maintain and expand margins—will remain under close scrutiny. For growth investors with a long-term horizon and tolerance for volatility, Nvidia could offer significant rewards. More defensive or value-focused investors, however, may wish to tread carefully or await further evidence of sustainable momentum as the AI race heats up and tech valuations recalibrate.

As always, performing rigorous research and weighing both the risks and potential remains the gold standard before making any investment decision.